Tariffs Tantrums Are Getting More Pushback Than Donut Holes

Goldman Sachs Now Sees Three Fed Cuts Later This Year

Recession Odds Are Rising Quite A Bit In Back Half Of Year

Mortgage Rates Could Slide More As Economy Receives Blunt Force Tariff Trauma

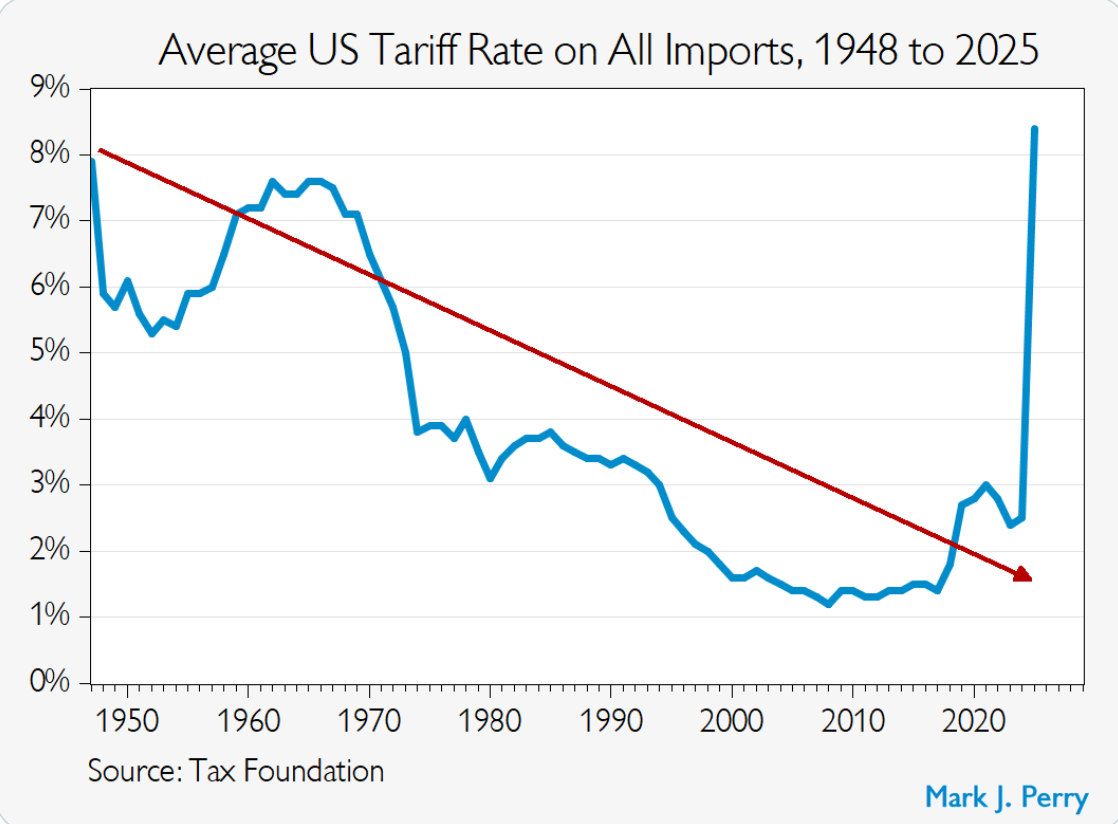

As I’ve mentioned here before, tariffs are inflationary, and that’s not a political statement. However, you can see in the chart below that the use of tariffs is significantly higher in Trump II than in Trump I, and that’s the point. Because of their much larger scale, today’s tariff threats wielded are not consistent or predictable. It prevents businesses from planning and budgeting. Consumer pushback and protests have been rising as have layoffs. Economists are getting more pessimistic about the once-solid economy. But what does this mean for the housing market and, by extension, mortgage rates? After all, I think I am supposed to be talking about this at some point.

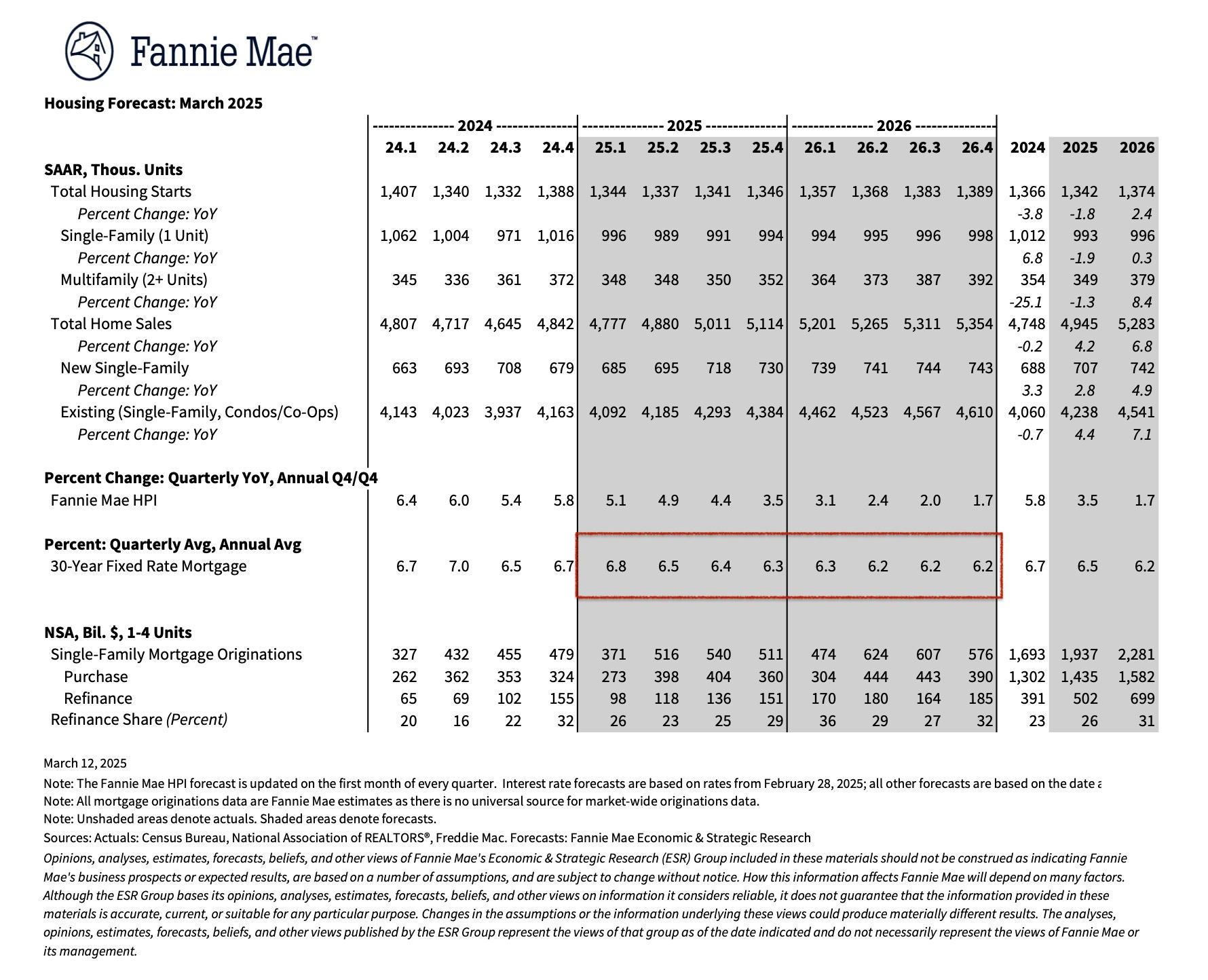

The scale of US tariffs threatened is the highest in more than 70 years. Let’s look at the result of the economic uncertainty they are creating. Fannie Mae’s 2025 housing forecast suggests slightly lower mortgage rates this year due to the weakening economic conditions, but nothing dramatic (see red rectangle on image below). Of course, that is dependent on whether the Tariff Tantrums dissipate in the near term and if there isn’t a lot more damage inflicted on the economy through the existing tariffs’ blunt force trauma. Tariffs have their use, but the incredible randomness of their application these days will be pretty damaging and probably help interest rates drop further. I’ve written about this before. It seems awkward to cheer for much lower rates as an assist to housing demand as it requires hundreds of thousands of people to lose their jobs due to a misunderstood economic policy that has limited credibility. It looks like economists think mortgage rates will drift to the low 6s in the back half of the year, which will probably drive more sales.

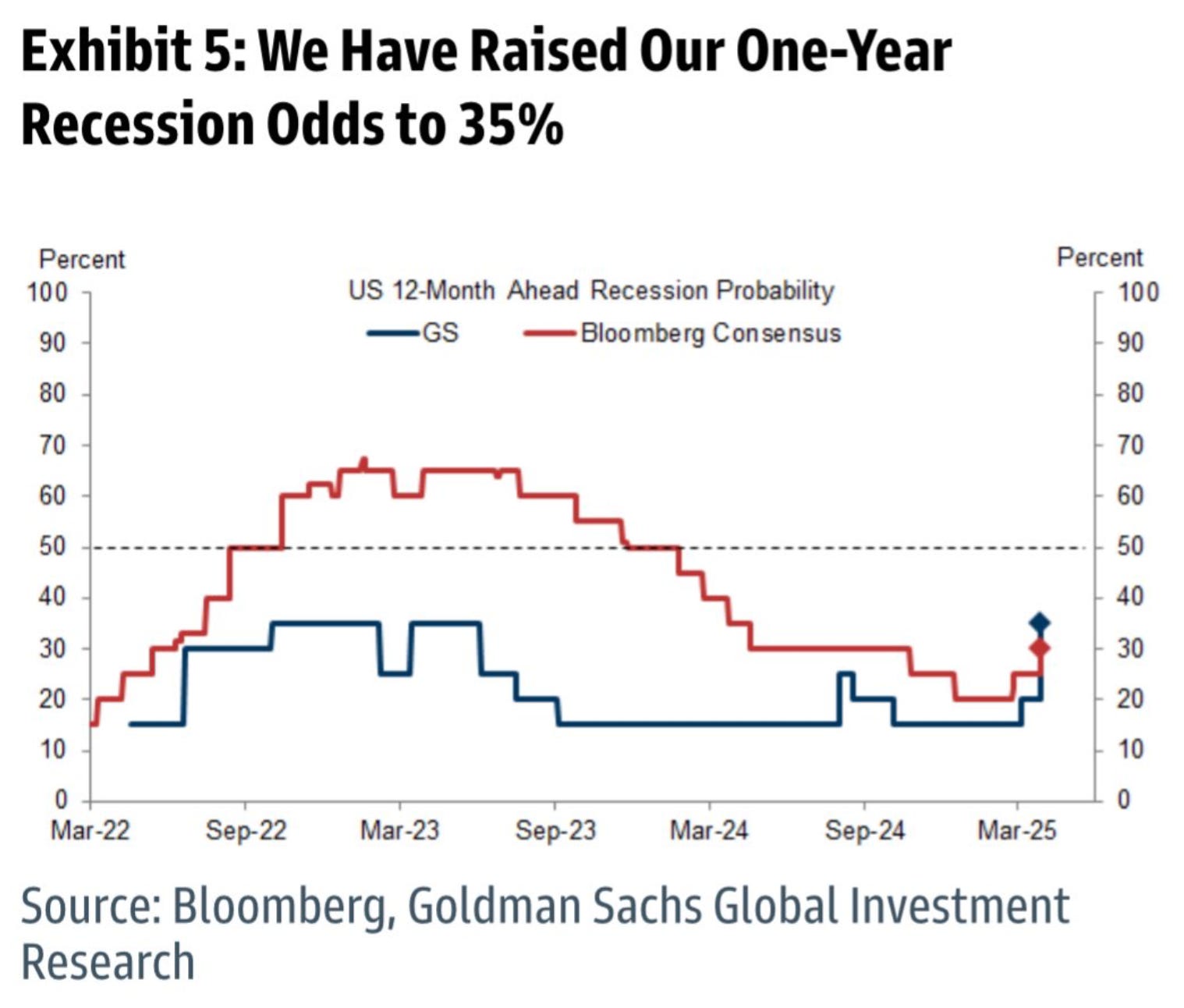

While a recession would bring lower mortgage rates, it would also cause lots of job loss. It’s probably tough to buy a home without a job, no? Goldman Sachs has seemed to be the voice of reason on recession odds over the past couple of years (blue line in the chart below), but even GS is showing much more concern about the impact of tariffs in recent days.

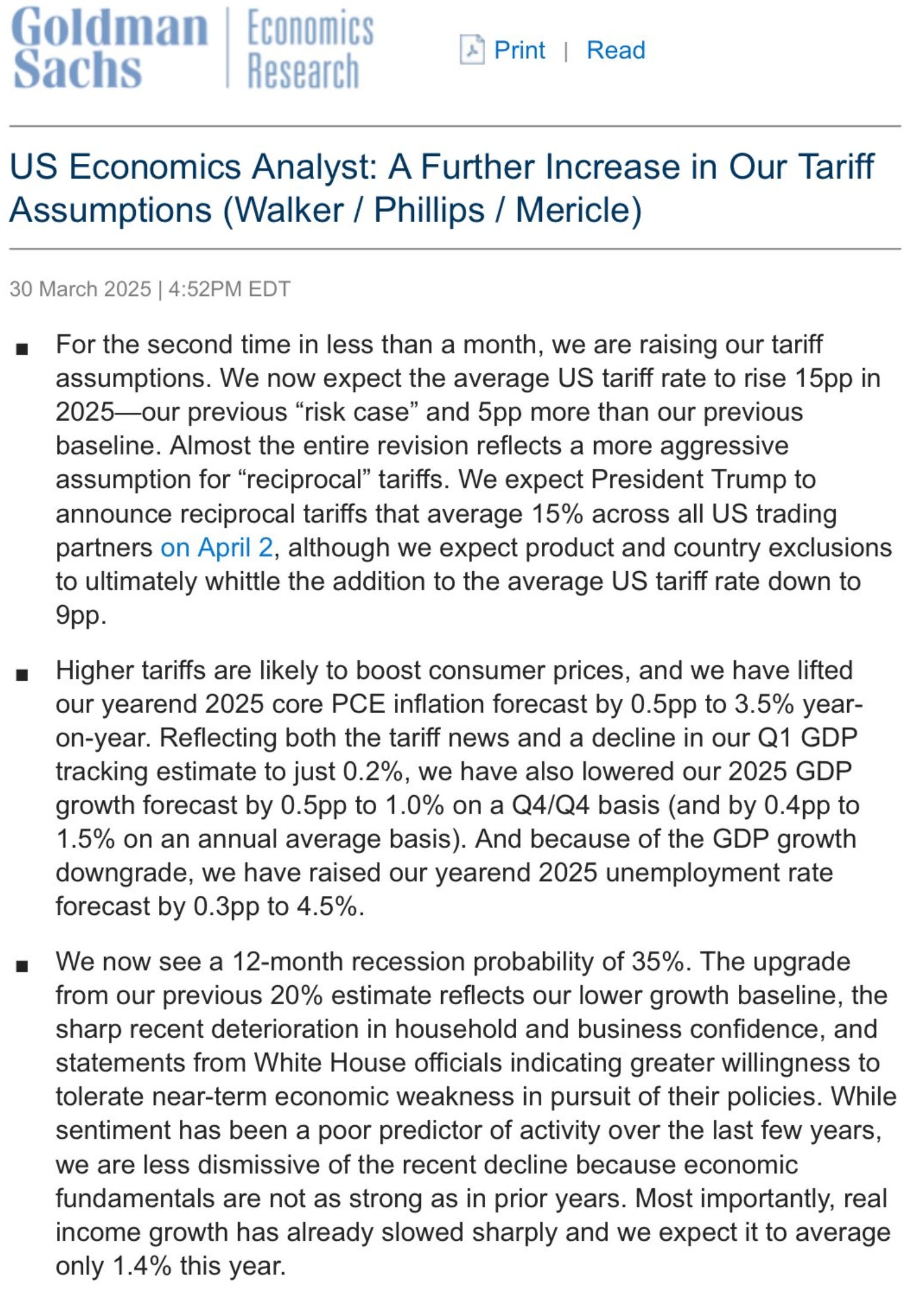

There’s no need to read the following note, but if you’re curious, it’s surprisingly accessible about tariffs with very little wonk.

Final Thoughts

Admittedly, I have been writing about tariffs quite a bit lately because they represent a significant challenge to a housing recovery. While their use seems random and has already proven damaging to the economy and financial markets, there is no sense of how long tariffs will remain front and center. The biggest question of the day is, “How will the housing market of 2025 compare to 2024?” We can’t make a reasonable determination, much the same as how companies are struggling with their budgeting and forecasting, unless one considers the US tariff plan, even though there doesn’t seem to be a US tariff plan.

Damaging the economy brings lower mortgage rates, and that’s probably good for housing if we don’t drift into a deep, dark recession with massive job losses. I’m using reason and logic here. Sorry about that.

The Actual Final Thought – Forget about tariffs. Who knew donut holes were something we could all agree on?

Appraiserville – today is a two-fer!

Appraisal Institute

Every so often, I need to check in on the governance of the appraisal profession because it does not disappoint. Bisnow published an explosive piece on the bad behavior of the Appraisal Institute, the appraisal industry’s largest trade group: Lawsuit Alleges Appraisal Institute Has Given States Fraudulent Test Results For Years. A few months ago, there was a rumor going around that their membership was collapsing (I’m not a member), falling from 17,000 to less than 10,000 post-pandemic, but they still report membership at 17,000. Now, with this latest lawsuit, Alissa Akins v. Appraisal Institute, the accusations of misrepresentation are certainly consistent with the membership count rumors and could complicate their defense.

Why should anyone outside of the appraisal industry care about fraudulent appraisal test scoring? Think about the US lending industry. Without credible state licensing, appraisers are not considered experts and not geographically competent. More importantly, the entire real estate lending universe is predicated on licensed and certified appraisers – trillions of dollars are lent every year on the value opinions of licensed and certified appraisers – if the points laid out in the lawsuit are accurate, the ethical failure of the Appraisal Institute presents a systemic risk to the US banking system. To those who know nothing about our industry, The Appraisal Foundation, which checks with the states to make sure they are compliant, has no enforcement powers. This situation has created a credibility clusterf**k for the profession.

I expect more lawsuits against the Appraisal Institute and, hopefully, the State of Illinois will chime in. Their toxic, corrupt culture that I’ve written about here since 2016, could bring them down financially as their membership is supposedly cratering. It creates the opportunity for fresh alternatives that help the appraisal industry rather than damaging it (as the current old guard has done so well). Now, think about all the Appraisal Institue executive flights with their emotional support spouses to Europe and Asia for no tangible reason, all on their hard-working members’ dime, which I used to write about here. Super Duper entitlements, I’d say (inside joke).

Appraisal Management Companies

Although Scott Reuters is a good man, his employer, Freddie Mac (along with the Appraisal Institute), is in bed with appraisal management companies [AMCs]. Why should you care? Instead of getting 10% of the consumer’s appraisal fee at mortgage application, AMCs get 50% to 70% and literally don’t add value to the mortgage process. With the now defanged CFPB agency and Fannie/Freddie looking to reduce the use of appraisers drastically, the consumer will continue to pay exorbitant appraisal fees that the appraiser doesn’t receive (AMCs lobby to hide this fact from consumers). Appraisers only receive 30% to 50% of the stated appraisal fee on a typical mortgage application. Shameful.

Monday Mailboxes, Etc. – Sharing reader feedback on Housing Notes.

March 28, 2025: Let’s Talk About The Weather Since Home Sales Are Augmented

If the tariffs actually happen, or if the uncertainty continues, I expect new home construction to slip. Materials prices are up significantly and I’m hearing of labor shortages because of the immigration crackdown. The uncertainty makes it hard for builders to plan, so the prudent plan is to pause.

Did you miss the previous Housing Notes?

March 28, 2025

Let’s Talk About The Weather Since Home Sales Are Augmented

Image: Gemini