Although I’m on vacation this week, I wanted provide a few thoughts on supply and demand (as in not enough vacation despite wanting more) with a dash of vomit (sorry). More on that later.

The high end luxury market is generally cooling across the globe because the world economic situation is changing. Developers are creating a whole lot of new luxury supply and governments are trying to get in on the action as a revenue opportunity.

Supply and Demand (and Monopolies)

I really love stories about supply and demand since it is so difficult for participants to envision the opposite conditions while the current conditions are in full swing. I mentioned my favorite lobster-related housing market post last week – a tale of easy credit and rejiggering supply. This week’s favorite is the vomit clean-up fee in Chicago taxis. A few years ago, Chicago introduced a new fare schedule with, of all things, a “Vomit Clean-up Fee.” This presumably was introduced to make visitors to that great city (I used to live there) feel better about not being hit with hidden charges. This idea is only something a monopoly would come up with. Can you imagine this item listed in a McDonald’s store menu? Ok, nevermind.

My anecdotal experience with taking a taxi from many U.S. airports shows a similar lack of enthusiasm for the customer. A dirty, cramped car with music blasting and air conditioning or heat barely reaching the back seat while I turn green has been my norm. Enter industry disrupters like Uber.

The biggest owner of NYC taxi medallions may see his empire collapse as a result of the combination of competition from Uber-type start-ups and high leverage, a reminder of the heady days of the housing bubble a decade ago. Tech startups like Uber and Lift [Lyft] have poached a huge market share of consumers from the traditional taxi medallion monopoly. I remember when Uber first burst onto the scene, a NYC medallion owner stated that it won’t have any impact on their business (I can’t find the quote but I literally laughed out loud). Over the past several years, the number of trips have fallen sharply and the only reason income is up 1% is because the city (a monopoly) raised cab fares by 17% a few years back.

I was listening to CNBC the other day and the topic was the Miami-Dade county housing boom. There are 43,000 new units (360 towers) slated to enter the market over the next two years. Do we think that will have an impact on the housing market? A friend and one of the best luxury brokers in south Florida, Senada Adzem Bernard, candidly lays out the scenario.

I was listening to one of my favorite podcasts this week, On The Media and during a segment on bogus health studies there was a terrific quote made that very much applies to housing market reports:

The Plural of Anecdote is not Data

Can there be a more applicable description of the misinterpretation of U.S. housing conditions? Here are a few examples.

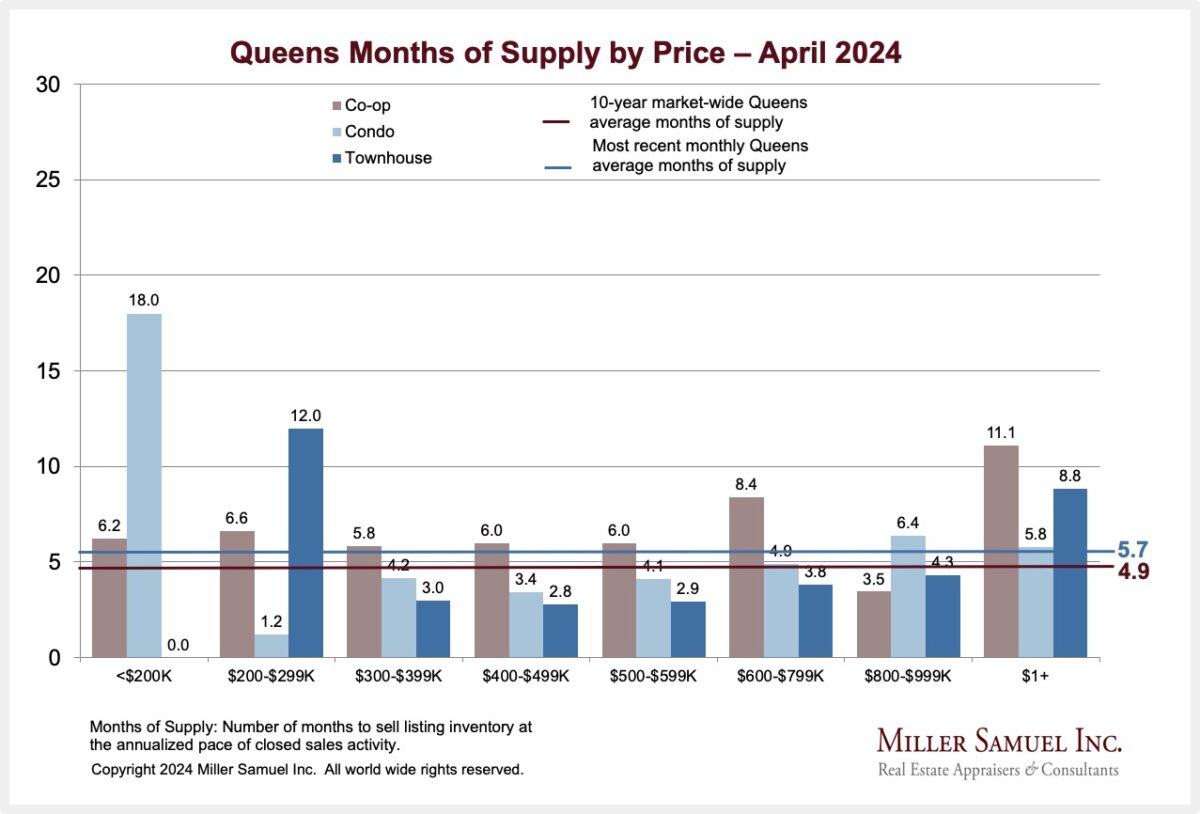

6 Month Absorption Rate I wrote about the “rule of thumb” adopted by the real estate industry that a 6 month absorption rate (the number of months to sell all supply at the current rate of sales) is the benchmark for a “healthy” housing market. In fact I’ve used it in the past before I looked into it. This NAR “benchmark” is based on nothing. Literally nothing. No research backs it up as a national standard. Plus it contradicts their other phrase “every housing market is different.’ Yet the 6 month benchmark is cited so often it has become fact to most in the industry.

Here are a few charts of absorption rates for some of the housing markets I report on.

20-City S&P/Case-Shiller Home Price Index No report is more misunderstood than Case Shiller. One of the creators of the index is a pioneer in housing trends and a Nobel laureate. However the index was actually created to allow Wall Street to hedge housing which is very logical but was a complete failure. This was because future results could be reasonably predicted. S&P continues to publish the monthly results because they love to publish indices. Unfortunately the results lag the actual market by about 6 months and the commentary around the results are based on anecdotal interpretation of lots of things that are not used to calculate the index, such as sales and inventory. My favorite S&P/Case-Shiller analogy (not anecdote) for the reliability of the index is to look at the average temperature 6 months ago and use that to decide what clothes to wear today. Silly.

David Blitzer, who is the public face of this index said:

First time buyers provide the demand and liquidity that supports trading up by current home owners. Without a boost in first timers, there is less housing market activity, fewer existing homes being put on the market, and more worry about inventory.

Yes, this is the sort of anecdotal fill in the gap analysis is what we should all be wary of since no part of the Case Shiller number crunching looks at this. Oh and this anecdote was refuted:

Research at the Atlanta Federal Reserve Bank argues that one should not blame millennials for the absence of first time buyers. The age distribution of first time buyers has not changed much since 2000; if anything, the median age has dropped slightly.

I have lost count of the number of times [pardon the missing graphics as a result of a hack of Matrix a while back] I have done a take down of the Case Shiller Index but here is an illustration of the time lag the index provides to consumers that is so misleading, especially when anecdotal explanations are used to fill in the gap (like above).

Let’s recap recent U.S. housing reports:

-Limited supply (not new development) pushes housing higher [Washington Post]

-New Home Sales Are Down [NY Times]

-Pending Home Sales Fall [Barrons]

-Existing Home Sales and Median Prices Hit Highs [Forbes]

Got it?

One Last Attempt to Sell a House Without an Agent

Yet another company, SQFTx Inc. is attempting to circumvent the real estate agent in the home buying process using “hip and current” techniques. LOL. (Hint: real estate tech bubble). FSBOs have long been a part of the market and the very idea that a large swath of the market would go this route is counter to my front line experience. In past cycles I have observed that periods with low inventory see an expansion of new FSBO tech initiatives while during slow downs FSBO start-ups tend to fall away as home sellers need more handholding because of the additional competition.

Of course my view on this is purely anecdotal. Back to vacation.

See you next week.

Jonathan Miller, CRP, CRE

President/CEO

Real Estate Appraisers & Consultants

ps Please feel free to share. If you get tired of all the charts, real estate commentary and articles presented in each weekly note, just opt out. I always appreciate feedback so please email me.

Must Reads

- Strong home sales, limited supply lift US home prices in May [Washington Post]

- Home prices rose 4.9% in May vs 5.7% increase expected: S&P/Case-Shiller [CNBC]

- Existing-Home Sales Hit Fastest Pace In Eight Years; Median Sales Price Hits New High [Forbes]

- More Weak Housing Data: Pending Home Sales Fall [Barrons]

- New Home Sales Slump to Seven-Month Low [New York Times]

- ‘Where the Renters Are’ Is a Look Into America’s Housing Crisis [CityLab]

- Selling your house without an agent sounds good. Is it? [Citizen-Times]

- Notting Hill Drops Most in London’s Luxury Home Market [Bloomberg Business]

- Episode 643: The Taxi King : Planet Money [NPR]

- Enjoying That Refreshing Blast of Cool Air on the Sidewalk? It’s Illegal [DNAinfo]

- Incurable American Excess [New York Times]

- Taxed Out of Mansions, London Investors Head Down-Market [Bloomberg Business]

- Sources say Bank of America sold LandSafe to CoreLogic [HousingWire]

![[27 Speaks Podcast] Jonathan Miller Provides A 2024 Hamptons Outlook](https://millersamuel.com/files/2024/02/27eastlogo-600x314.jpg)

[…] dissing the relevance of the S&P/Case Shiller Index because of the 6 month lag and the slew of anecdotal link-the-dot official commentary associated with it that literally has nothing to do with the numbers generated (gasping for air). […]