Surfside Condo Collapse Spurred Law and Rule Changes

Many Condos Were Deemed Unsafe, And Developers Tried To Buyout Owners

Recent Lawsuit In Florida Has Frozen Condo Terminations, Creating Zombies

Part of the ownership structure of a condo unit is the legal concept that the association can overrule what an individual unit owner desires. The opportunity to decommission older condo buildings accelerated with the Surfside Miami condo collapse in 2021. Municipalities, regulators, and banks took a hard look at condo associations that had the ability to avoid making major repairs because of their inherent conflict of interest. Such a conflict resulted in skipping structural repairs to save money, ultimately leading to the death of 98 people at Champlain Towers South.

I remember seeing the first video of the condo collapse and watching it over and over again, wondering what I was actually seeing. I wondered what the condo association and the board members (who were still alive) thought about the tragedy after fighting to defer structural repairs all those years. This was a classic case of placing safety compliance rules in the hands of an entity (the association) with a conflicting self-interest of not wanting to pay for it.

Municipalities immediately performed reviews of condo structures for safety in the region, and many older condominium buildings were subsequently evacuated. Fannie Mae tightened its requirements, and developers recognized the opportunity to build new condos.

The problem here is that the math for new development generally only works for luxury-type products. High land costs and high development costs push new products towards luxury. The older condo housing stock represents the affordable segment of the market, and as it ages, it is likely to continue to shrink over time. Bankrate talked about the new GSE rules last year, which are now permanent.

Fannie Mae and Freddie Mac, the two government-sponsored enterprises (GSEs) that back much of the U.S. mortgage market, have made some temporary condo loan rules now permanent.

The guidelines, established in response to the Surfside, Florida, condo collapse, preclude unsafe communities from GSE financing.

The rules help protect buyers from obtaining a mortgage for an at-risk condo. For some, however, they could also limit loan options.

These rule changes mean that unit financing for developments that are within the range of Fannie Mae’s conforming loan amounts goes away, and buyers need to pay cash, pay hundreds of thousands in special assessments, or can’t refinance, presumably resulting in a significant value discount. Fannie’s actions realign the financial incentives of the market with the safety of residents. It’s unfortunate because with all the deferred maintenance, someone has to pay to catch up, and the association member will not have to pay for deferred maintenance over the years. That’s the other tragedy in this situation.

My developer description and why I wouldn’t have the stomach for it: “Developers develop until they can’t develop anymore. It usually ends badly, but 5 years later they start over like nothing bad ever happened.”

With the lack of choice of waterfront parcels, the old concept of taking over an older condo project – condo terminations – became a more popular option. They buy out the units for above market price and then gain control of the association to dissolve it, which has been gaining momentum as a byproduct of the Surfside catastrophe. At least 26 South Florida condo buildings were deemed unsafe a year after Surfside.

A month and a half ago marked the third anniversary of the Surfside tragedy. Here’s a good recap.

Bombshell Court Ruling Freezes All Stakeholders

About six months ago, a handful of condo owners in a 191-unit building at Biscayne 21 won a lawsuit on appeal – they refused to sell their units and didn’t want to be forced out of their homes. The unit owners had turned down buyout offers from the developer that were much higher than what they paid for their homes originally, but that wasn’t the point. They didn’t want to leave their homes.

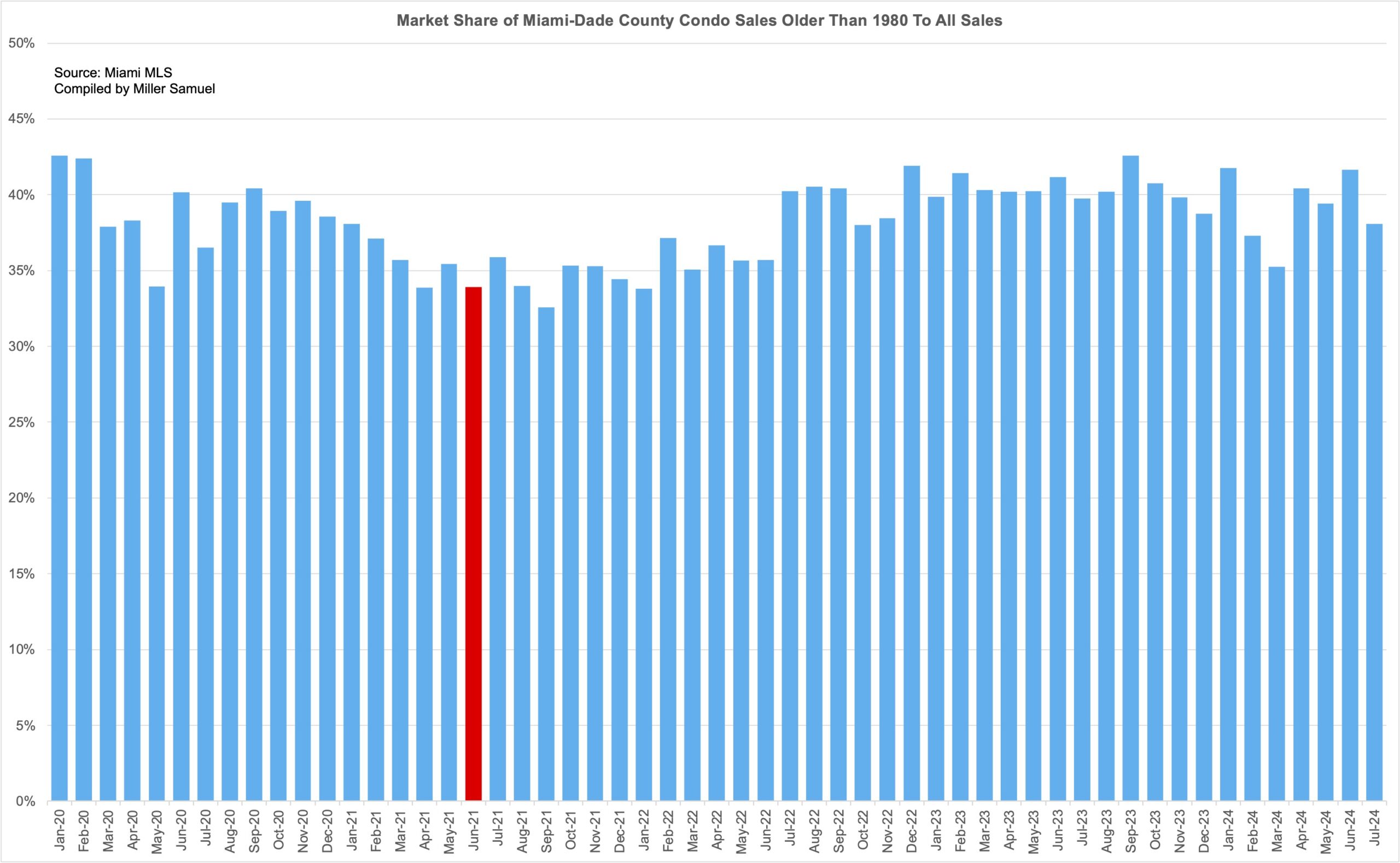

I took a cursory look at Miami-Dade County condo sales before and after the June 2021 Surfside tragedy, tracking the market share of sales older than 1980 (the Surfside building was constructed in 1981) versus all condo sales. The results were not telling. If anything, the market share of old sales rose after the tragedy. It makes me wonder if this reflected the pressure to purchase lower-priced condos with the spike in mortgage rates since 2022. If there is a better way to look at this, I’m all ears.

The developer had already turned off utilities, and the building occupants, including the plaintiffs, had already moved out. The victory on appeal was shocking to the development community, and without precedent, everything now is on hold. This will cause a lot of concern among developers regarding other condo terminations in process. I don’t know what the basis of the appeal’s win logic is yet, but the situation will have to be cleaned up or legally resolved before other condo terminations are initiated.

In this case, with the results of the appeal, all the stakeholders are stuck. The developer has borrowed money for the conversion, and many of these buildings are unsafe or require a lot of repairs. Now, the developer can’t convert until the legal issues are resolved, and that takes time. The unit owners have already moved out.

How Did The Unit Owners Get Here?

It wasn’t about the price.

Developers tend to offer above market-rate prices for the earlier sales. But once they reach a certain threshold needed to terminate a condominium through a vote—often 95%—the remaining owners are compelled to sell.

Wall Street Journal

The final 5% of the units are appraised using a specific process, but the appraiser can’t look at what the other units were purchased for (often can be at a premium).

That is why this development is now referred to as a Zombie condo. Its existence will delay similar planned terminations and place much doubt on the process in the future. This decision could potentially spread to other U.S. markets and will get the attention of Fannie Mae. I’m not a lawyer, and I don’t fully understand if there are any legal options for developers. However, I find it odd that, in my understanding, this type of fee simple ownership has largely been a majority rule concept, and owners must understand when they buy into one. A small number of people under condo rules can turn a development into a zombie stuck in time. For now, this could potentially damage the condo concept as a form of ownership.

A Hamptons media outlet I pay attention to is 27east of the Southampton Press and they have have invited me over the past several quarters to speak with their editors [...]