Twist and Shout: Fannie Says Sales Sentiment Is Ho-Hum While Toll Brothers Says Luxury Is Ready To Rock.

Current GSE Forecasts Are Dated. Based On Old Expectations Of A 25-Basis Point Cut

Anecdotal Data Bridges The Lag In Actual Data Usually Relied On For Trends

High End Housing Continues To Outperform The Balance Of The Market

We are in the middle of a cross-over period on housing market expectations. The July indices being released were tracked before the financial markets’ yen carry trade turbulence in early August, which raised expectations for more significant Fed rate cuts. Fannie Mae crafted their negative outlook on housing sales, which came out today on their Home Purchase Sentiment Index for July. Their index doesn’t consider the very recent pivot in rate cut expectations. Freddie Mac, the privately traded weaker sibling created in 1970 to foster competition (but mimicks publicly traded Fannie Mae’s moves), sees the same weak sales picture. Yet the luxury home builder Toll Brothers expects a significant uptick in profits as a result of higher rate cut expectations – they saw tangible evidence of higher traffic this month (August), which would translate into more sales (and a higher stock price).

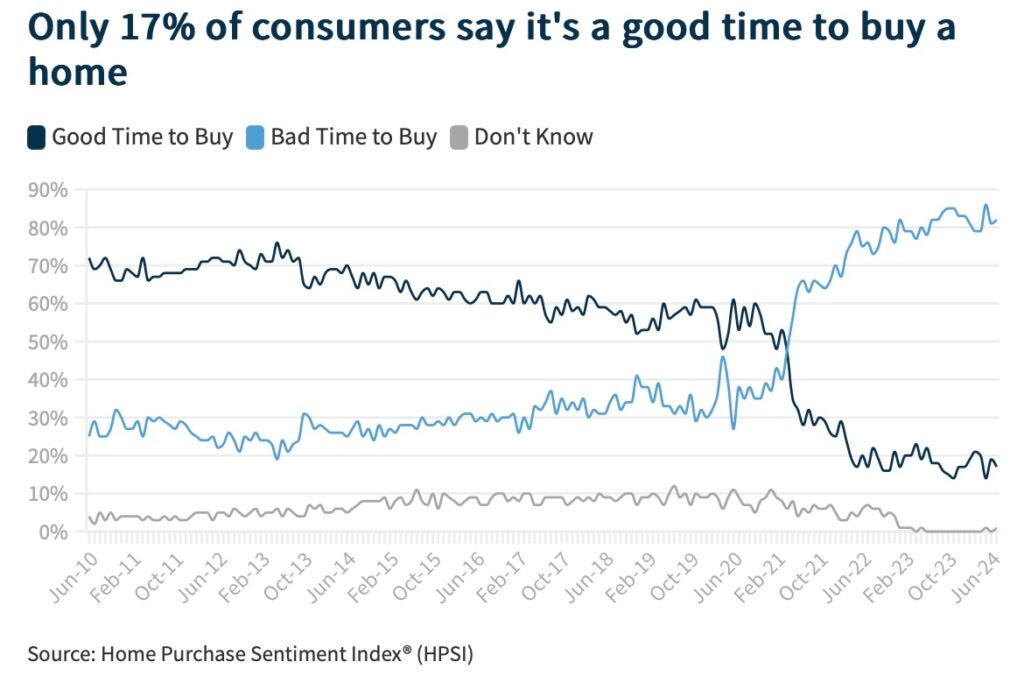

I spoke about “sentiment” a few days ago in As We Consider Confidence Versus Sentiment, Remember That Swearing Lengthens Our Lifespan. Fannie Mae saw consumer sentiment in a very negative light in July.

However, NAR’s existing home sales rose for the first time in four months, aided by a 20% rise in listing inventory. The report also shows that conditions are better at the higher end of the market, and cash buyers are up as well. This expansion in activity occurred primarily from May and June Contracts, well before the yen carry trade and the pivot in expectations to larger rate cuts.

Of course, I would be remiss if I didn’t point out that Toll Brothers is looking at the high end of the housing market, and the government-sponsored entities (GSEs) tend to look at the meat and potatoes of the U.S. housing stock, given their caps of the mortgage sizes they buy or guarantee. This difference in outlook may also explain some of the outlook’s disconnect, but not much.

Anecdotal Evidence Connects The Actual Dots

From the Internet years ago, so it must be true: “The Plural Of Anecdotal Is Not Data.”

The problem with surveys and reports (which I produce for a living) is they can’t reflect sudden shifts in market conditions. These tools eventually catch up to anecdotal evidence but seemingly contradict the event as it is actually happening. I connect the dots through the insights I share within the report itself. In the case of Fannie Mae’s outlook, even though their chief economist, Doug Duncan, is one of my favorites, they were focused on July sentiment results that didn’t reflect the current reality of the worry-bead clutching of early August from the yen carry trade.

As I mentioned in a previous post about sentiment, it accounts for how consumers feel about the future and less about the present. A pivot in expectations about rate cuts could change future expectations about home sales. While I’m not suggesting that the majority of consumers will have a wildly positive sentiment toward home-buying in August, I would expect a shift to higher home sale expectations in Fannie’s next forecast.

The power of anecdotal information is that it can help guide toward a new direction until the empirical evidence catches up. Case in point – I’ve been interviewed for the Federal Reserve’s Beige Book for more than 15 years. I love this resource for housing market participants because it provides an anecdotal take on different aspects of the economy with the idea of giving clues to future results. Now, the big talking point by the Fed is that they are waiting for the data until they make a move. That, by definition, means they lag actual conditions and aren’t relying on anecdotal takes on the economy such as the Beige Book provides, and it probably took an odd event like the blow-up of the yen carry trade to change the expectations of future rate cuts.

Sometimes I feel like John Lennon did when yelling into a screaming crowd, substituting the expected “Twist And Shout” with the more anecdotal “I’m pissed with gout.”

Did you miss yesterday’s Housing Notes?

August 21, 2024

The Proliferation Of Air Conditioning Has Homogenized Our Homes

Image: Chat & Ask AI