Conventional wisdom says that a flattening yield curve infers a recession is imminent.

While I don’t surf, ever since I read Barbarian Days: A Surfing Life, I relate to surfing analogies. Here’s the way I see it (hint: I can’t see it):

Yahoo Finance TV 12-4-2018 – Toll Brothers & Banking Conditions in Real Estate

I was invited by Julie Hyman at Yahoo Finance TV for a discussion on the weakening luxury housing market and some other topics of interest. I’ve known her for years, after a long run at Bloomberg TV, and am excited about her new opportunity at Yahoo.

When I arrived at the studio, the stock market was being battered (down by over 400 points at the time of this broadcast) by the conflicting interpretations of the recent US/China tariff talks and the results Toll Brothers analyst call. It was exciting to be there during the perfect storm. The conversation shifted from what I was invited to cover, to the developing news story.

Yahoo is ramping up live coverage in early 2019 via 100% internet. Judging by their super cool/huge studio and throngs of people working there, Verizon seems very serious about their investment.

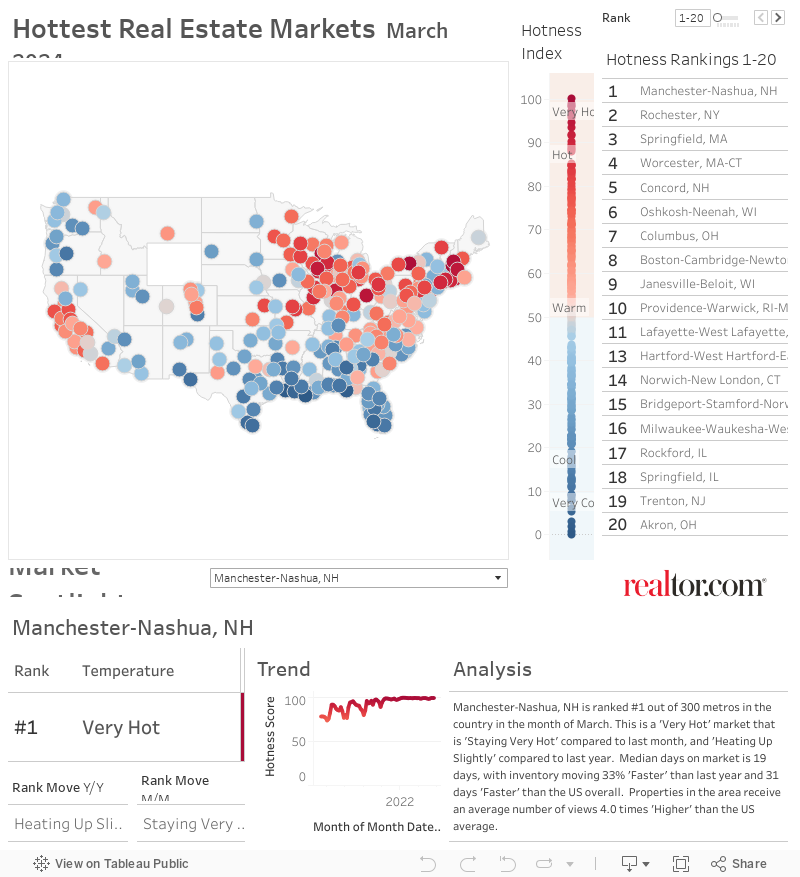

New in the Real Estate Lexicon: Hotness

Realtor.com, not to be confused with the National Association of Realtors as an interesting resource called the “Market Hotness Index” that tells you how “hot” your housing market is.

This naming decision feels like me telling one of my “dad jokes.” I think I am on point but my wife and kids just roll their eyes to which I use “got woke” in a sentence and only make it worse. Other than that, it’s a fun tool to play around with.

Every Housing Notes Subscriber Should Sign Our Petition

The valuation business sits on a three-legged stool which stand for quality, cost and speed. Since the financial crisis the regulatory world has been obsessed with speed and cost of appraisals, and championing the deeply flawed execution of vehicles such as appraisal management companies (AMCs), misrepresentations about hybrid appraisals and automated valuation models (AVMs). At no time is the topic of quality broached. For the regulatory entities such as the Federal Reserve, US Treasury, FHFA and OCC, the objective seems to be to goose more mortgage volume out of the system since falling mortgage rates didn’t seem to bring more volume (hey, that’s a sign. Many agencies depend on fees from the banks and with the moral hazard established by bailouts of a decade ago, the taxpayer is always a backstop when things go wrong. Hence the illogical pursuit of eliminating appraisals, who account for ±.02% of a transaction but are the only non-biased resource in the entire mortgage process.

If this is too much acronym gobblygook for you to understand what I just said, just understand this: the economy is drifting towards recession. Whether it does tip into a recession is not guaranteed but the housing economy is clearly cooling as evidenced by slowing sales and rising inventory. How did turning a bling eye to quality work out a decade ago? We are still in the financial crisis hangover as evidenced by unusually low rates. The regulators are trying to pull more mortgage volume through the pipeline by cutting all costs and speed that no consumers are screaming for.

While I have no expectations that signing a petition will stop what has been predetermined, I do hope it catches the attentions of lawmakers. I hope we won’t have to look back a few years from now and wonder why we didn’t do anything about this before it was too late.

This is only a first step and its important. Please sign now to make your voice heard:

Remember liar loans of a decade ago? Those same people want to do away with appraisers. [Change.org]

Here is the FDIC announcement on real estate appraisals.

And my take on the matter in REALTOR Magazine. All real estate agents are exposed to significant risk if this rule change is adopted. The same people in power during the era of liar loans are pushing for this rule change.

Getting Graphic

Some of my favorite charts of the week.

The problem with the messaging here is that within urban markets, there was a massive amount of development, yet the narrative about lack of building pertains to single family homes. The problem for both suburbia and urban markets is that that the product built was heavily skewed to luxury, which exacerbated the shortage and why we have a national affordable housing crisis.

LIC Survey

Appraiserville

(For earlier appraisal industry commentary, visit my old clunky REIC site.)

I’m visiting family in Colorado at the moment, going to see my nephew play Division 1 NCAA college basketball so I’m holding off on Appraiserville commentary this week. Although take a look at the additional commentary surrounding the petition early in Housing Notes – all of you really should sign the petition if you haven’t already.

OFT (One Final Thought)

Sometimes…things change in a second.

That was close. pic.twitter.com/GukrT5wHsX

— Caught on CCTV ???? (@CaughtCctv) November 15, 2018

Brilliant Idea #1

If you need something rock solid in your life (particularly on Friday afternoons) and someone forwarded this to you, or you think you already subscribed, sign up here for these weekly Housing Notes. And be sure to share with a friend or colleague if you enjoy them because:

– They’ll petition;

– You’ll show Hotness;

– And I’ll watch people surf.

Brilliant Idea #2

You’re obviously full of insights and ideas as a reader of Housing Notes. I appreciate every email I receive and it helps me craft the next week’s Housing Note.

See you next week.

Jonathan J. Miller, CRP, CRE, Member of RAC

President/CEO

Miller Samuel Inc.

Real Estate Appraisers & Consultants

Matrix Blog

@jonathanmiller

Reads, Listens and Visuals I Enjoyed

- The U.S. Yield Curve Just Inverted. That’s Huge. [Bloomberg]

- Nearly One in Three Homes For Sale in October had a Price Drop—Highest Level Since at Least 2010 [Redfin]

- The Major Challenge of Inadequate U.S. Housing Supply [Freddie Mac]

- Risk is building in the housing market [American Banker]

- Flatter Yield Curves Aren’t Always Bad News—but This One Is [Wall Street Journal]

- CoStar News – House Republicans Push to Ease Property Appraisal Rules Before Giving Democrats Control [CoStar]

- Does the Yield Curve Really Forecast Recession? [St. Louis Fed]

- 3 charts suggest housing ‘bubble trouble’ with a tech meltdown ‘yet to come’ [MarketWatch]

- The Reason Many Ultrarich People Aren’t Satisfied With Their Wealth [The Atlantic]

- The Housing Slowdown Is Here—and These 10 Cities Are Getting Hit Hardest [Realtor.com]

- Federal Reserve: More homeowners are getting their refi applications rejected [Housingwire]

- 2018 US Labor Market Review and Outlook: When and How Will Good Times End? [Indeed Hiring Lab]

- The Mayor Bringing Other Mayors Together around Housing [Next City]

- New Robert A.M. Stern Condo on Park Avenue Sells for Nearly $74 Million [The New York Times]

- Existing-Home Sales Suffer Largest Annual Drop in Four Years [The Wall Street Journal]

- New-home sales fall to a nearly 3-year low; inventory surges as housing-market outlook darkens [MarketWatch]

- Market Hotness Index [Realtor.com Economic Research]

- Visualizing the Aftermath of the Real Estate Bubble (2007-17) [howmuch.net]

- My luxury rental building is converting to condos. What can I do to stay in my apartment? [Brick Underground]

- N.Y. Today: Protecting Rent-Stabilized Tenants From Shady Landlords [The New York Times]

- Sorry, home appraisers, bots are coming for your jobs [The Real Deal]

My New Content, Research and Mentions

- Eliminating the Appraiser! Remember Liar Loans of a Decade Ago? [Jonathan Miller/Appraisers' Blog]

- The average size of an apartment in America is shrinking [Daily Mail UK]

- Going Commando Under $400K: the Death of the Home Appraisal? [CandysDirt.com]

- 金融海嘯時隔10年 9州房市仍未全恢復 [Sing Tao USA]

- Toll Brothers Inc. reporting its first drop in orders since 2014 as luxury real estate market cools [Yahoo! Finance]

- In Manhattan things are soft and getting softer. Is it a Melbourne style price free-fall? Not yet…but getting there. [Investment Watch]

- Stocks slide over mixed messages from White House [Yahoo! Finance]

- Housing market cools, and Toll Brothers outlook shows luxury hit hard [CNBC]

Real Estate Blockchain Reads

Appraisal Related Reads

- Why Appraisers? [Birmingham Appraisal Blog]

- U.S. push to cut back on home appraisals sparks controversy [Florida Realtors]

- How Do We Find Accuracy? [George Dell]

- Just Don't Do It [Comstock's Magazine]

![[Podcast] Episode 4: What It Means With Jonathan Miller](https://millersamuel.com/files/2025/04/WhatItMeans.jpeg)