Abused For Years, The Zeigeist For Real Estate Appraisers Might Be Changing For The Better

Time to read [10 minutes]

NYC Managing Agents Are Gouging Applicants With High Info Fees Needed To Buy

Pulte Pauses Freddie and Fannie’s Privatization After Inferring Certainty

The ASC And TAF Are Under A Lot Of Pressure To Change

I’m overdue for a recap of the residential appraisal world of mortgages which impacts many participants in the home buying process. Years ago, an experienced real estate appraiser once told me, “In a home sale, everyone knows the ‘number’ before the appraiser arrives on the scene. The real estate agents on both sides, the attorneys on both sides, the buyer and the seller and the mortgage brokers all know what the sales price should be because their compensation depends on it.” The appraisers are the only neutral party in a sales transaction, yet they are constantly under siege.

Managing Agents In NYC Are Gouging Appraisers

When performing appraisals in urban markets, appraisers often have to contact the managing agent of the condo or co-op building to get information from them to supplement public record. Typical fees for such inquiries used to be less than $100 and we built it into the appraisal fee from the bank. Then the standard fee doubled to $200 and then $400 and now we are starting to see $600 fees quoted all in the past couple of years. A few years ago when the economy saw a spike in inflation, it looks like this industry is taking advantge of the fog it created about pricing. Or I’m just spitballin’ here but suggesting that managing agents got together and agreed to raise the fees singificantly at the same time.

In some ways, who can blame the management companies who manage buildings on razor thing margins and who end up being the punching bag for the unit owners they represent. The rationale for owning a management company used to be that it generated referrals to real estate brokerages for future sales commissions. For example, when a unit owner passed away, the managing agent lets the real estate agent know that an estate sale is probably on the horizon.

But appraisers are now caught in the middle. If the appraiser quotes a fee of $1,000 for an appraisal to a bank for a refinance, and the managing agent suddenly ups their fee from $100 to $600, banks don’t want to absorb the additional cost, so they expect the appraiser to eat the fee. This fee explosion is happening every day. My quoted fee of $1,000 is now $400 after paying for the $600 managing agent, which is not sustainable. I am fortunate that we perform thousands of Manhattan appraisals per year, and a large chunk of that work occurs multiple times in the same building. I can sometimes suss out the missing information. However, I can’t absorb the extra cost on all orders if I do not have the data needed. In that case, I can either decline to complete the appraisal assignment or complete it without the updated information and add a lengthy disclaimer. The bank is in a perfect position to demand the information from the mortgage applicant. Still, with all the cutbacks and low volume, banks and mortgage brokers are operating on thinner margins these days, too, despite having access to databases and digital information. Many managing agents are now opting to gouge everyone for information that takes five minutes to retrieve.

I understand, but the appraiser is the one who must balance the economics of survival with the ethics of reliability. We remain the lone wolf of the home mortgage process, but walk into a wolf’s den on nearly every assignment. I like that metaphor!

Pause On Fannie Mae And Freddie Mac Privatization

FHFA Chair Bill Pulte has decided to pause the privatization (releasing them from government conservatorship) of GSEs after building up expectations that this action was a given. I contended that with trillions of bonds backing the housing market, this would cause mortgage rates to tick higher because the government’s guarantee as a backstop would no longer be a sure thing. Additionally, there has been no meaningful discussion on the impact this action will have on the housing market. I assume Pulte recognizes the inflationary pressures already being imposed on housing by tariff policy and the trade wars. In addition, Fannie Mae has long made inferences that bank appraisers will no longer be needed, relegated to data collectors. Such a move also puts more risk into the system when an AVM can’t adjust for the 500 feral cats that have been living in the home for three years. At the same time, valuations would be automated, as in Automated Valuation Models (AVMs) such as the Zestimate. Perhaps the pullback from privatization is a temporary respite for appraisers.

Appraiser Regulator Chaos

Sasha Jones, reporting for Bisnow, has been extensively covering the regulatory landscape of appraisers over the past couple of years. Her piece explains the current malfunction: Senators Say Appraisal Regulator ‘Chaos’ Risks Undermining Real Estate Markets. Two U.S. senators wrote to the Federal Financial Institutions Examination Council (FFIEC), inquiring about the Appraisal Subcommittee (ASC), which has been weakened under the current administration. I testified in front of the ASC in Washington, DC, a few years ago, before the current administration gutted it.

UPDATE Her followup piece: Appraisal Subcommittee Head Departs Amid Trouble At The Agency

Defunding The Appraisal Foundation Is Bipartisan

There is an effort in the Senate to cut funding to the Appraisal Foundation by half, which makes sense given the entirety of its bloated budget and disconnect with the appraisal industry. They are primarily responsible for driving us into the ground as a profession by aging us out.

Here’s a little stroll down memory lane. Before I testified in Washington about TAF’s bureaucratic burden on the appraisal industry a few years ago, the Consumer Finance Protection Board (CFPB), the ASC and many other regulatory agencies read my Housing Notes every week for the latest explanations on the meaningless accomplishments of checklists created by former TAF president Dave Bunton to show he was doing something. He actually stated that I was a liar in his testimony to the ASC and that I have a problem with the truth, all of which was said while he was lying. It was epic, and I received a tsunami of congratulations from agencies and professional colleagues for shaking up his grip on the profession, prompting him to retire a few years earlier than his contract suggested. With TAF’s uselessness and ASC defanged, appraisers are left to their own devices. With Fannie Mae planning to push bank appraisers out through debunked automation, some hope is emerging.

A Senate Bill, the “Appraisal Industry Improvement Act,” was introduced last May that would essentially cut TAF revenue by half. Here is a good summary of the bill, which adds trainees to the national registry. This bill would remove TAF’s crippling requirement, which makes hiring trainees a non-starter, and instead rely exclusively on the mentoring system. In our appraisal practice, we must wait 2-3 years before a trainee becomes cost-effective to hire, so we essentially can’t hire new staff to perform bank work. Throw in AMC appraisal fees at 50 cents on the dollar of market rates, and we really can’t do much bank work. TAF stupidly engineered this, so we need fresh takes on the future of our profession. Being on decorative committees to pad one’s resume doesn’t move our profession forward. The bill also adds the VA to the ASC, which is long overdue.

Final Thoughts

My appraisal industry continues to be under siege but there is some hope on the horizon as seen in recent proposed legislation. The idea that I can’t hire appraiser trainees and use them for up to three years is ludicrous. The idea that appraisers have to eat costs for information required by banks and the banks don’t want to cover the costs is unfair to my profession as well.

Still, with all the uncertainty and insanity floating around the home buying world, particularly in the mortgage process, I feel more optomistic about the long term outlook than I have in a while. We need a fresh look at the future.

The Actual Final Thought – How appraisers should respond to clients giving them grief about their fee quote. One more thing – Tom Lehrer was a massive hit in the 1950s and 1960s. I first heard “Poisoning Pigeons in the Park” and “The Old Dope Peddler” in the 1980s and proceeded to install all his music on my iPhone alongside my punk rock music collection. I have an eclectic ear at best, but it’s a guilty pleasure to listen to musical satire of a different era, set against the social mores of the time. It helps me attempt to imagine what the current era will sound like in a few decades.

[Podcast] What It Means With Jonathan Miller

The Technology And The Housing Hype Cycle episode is just a click away. The podcast feed can be found here:

Apple (Douglas Elliman feed) Soundcloud Youtube

Monday Mailboxes, Etc. – Sharing reader feedback on Housing Notes.

July 25, 2025: Why On Earth Would Someone Buy In A “Ground Lease” Building?

Yes, why would you buy a land lease property? In South Scottsdale, there are several land lease subdivisions which provide low cost residual income for heirs of founding families in the area. Herberger Family owns some for example. The condo townhouses along one of the golf courses at the Phoenician (Charles Keating developed the famous resort) were land lease properties until about 10 years ago. I know of one subdivision of Briarwood where listings advertise a buy out option. You’re right, the HOA includes the land lease portion and the properties sell at a discount to fee simple and they are high. These subdivisions were built out in the 70s and 80s and are centrally located to entertainment and shopping in the area.

However, these residential subdivisions are overshadowed by the Salt River Pima-Maricopa Indian Community land lease properties. A stretch of the 101 freeway is built on Native lands and since the corridor is central, it is a hub for tourism including tribal casinos, Top Golf, Odysea Aquarium, etc. Plus, there are many non tribal businesses that operate on native land leases. Target and Walmart, Home Depot, Michael’s Crafts, Hobby Lobby, an Autoplex car dealer mall, gas stations, fast food, offic parks etc. operate on Salt River lands. Interesting fact, alcohol isn’t sold on reservation Target and Walmart. As the area grows, it will be interesting to watch the development of tribal lands. Much of the corridor is still agriculture but each year, more projects break ground. You can see on the map how vast the reservation lands are and so is the opportunity for the tribes. https://srpmic-nsn.gov/about/area-map/#:~:text=How%20to%20Find%20the%20Salt,prominent%20cultural%20and%20geographical%20landmark. I used to think land leases were just in Hawaii, but they’re common here.I like your take on the ground lease

Thanks for this blog! In the course material for my teaching “The Appraiser’s Guide to the New URAR”, (7 hr CE class) the topic of condo & coop leaseholds comes up. Frankly, I don’t spend any time discussing this because out here in WA we don’t have any (that I know of…and other appraisers concur when I ask.) But your explanation helps me know more about this segment of real property appraising. We do have leasehold properties on Native American Tribal Reservation areas, so I mention those with more time spent.

Did you miss the previous Housing Notes?

July 25, 2025

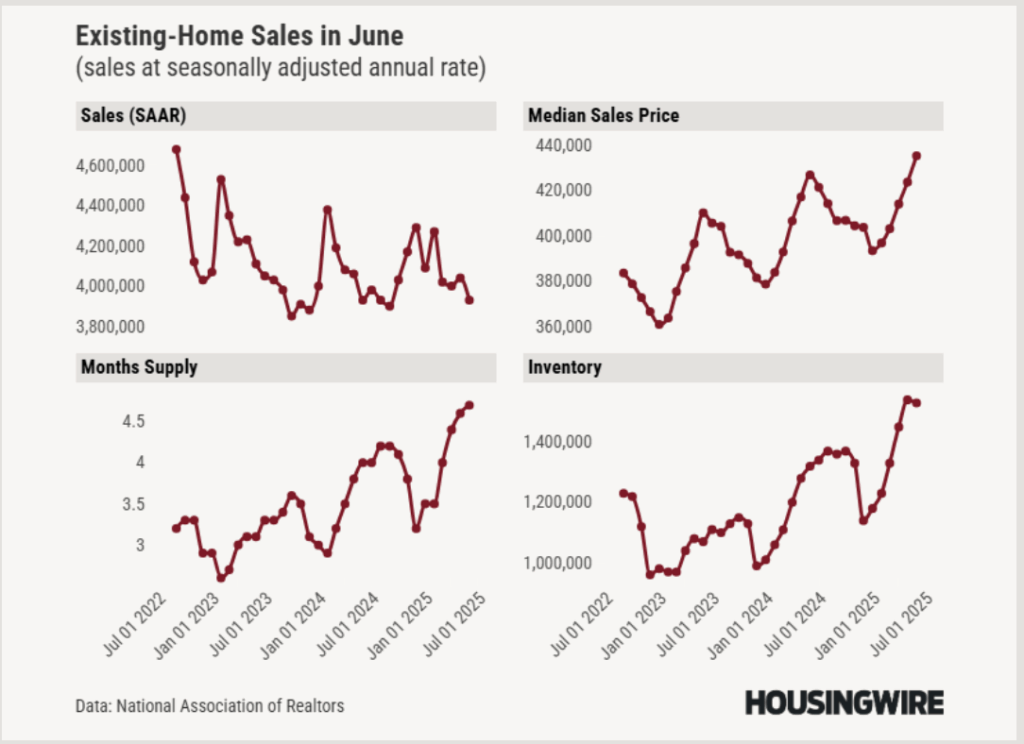

Sales Are Down While Mortgage Applications Are Up

Image: Housingwire